Week in Review: Four Fabulous and Not-So-Fabulous F-Words

This week in macro was brought to us by the letter F.

Fiscal

First, there was the celebration over the impact of Big Fiscal policy on the U.S. economy. Hallelujah!

It wasn’t all that long ago that leading economists were arguing that the Trump tax cuts had so wrecked the nation’s finances, that it would be next to impossible for Congress to fire off enough fiscal support to thwart an economic downturn. That was obviously wrong.

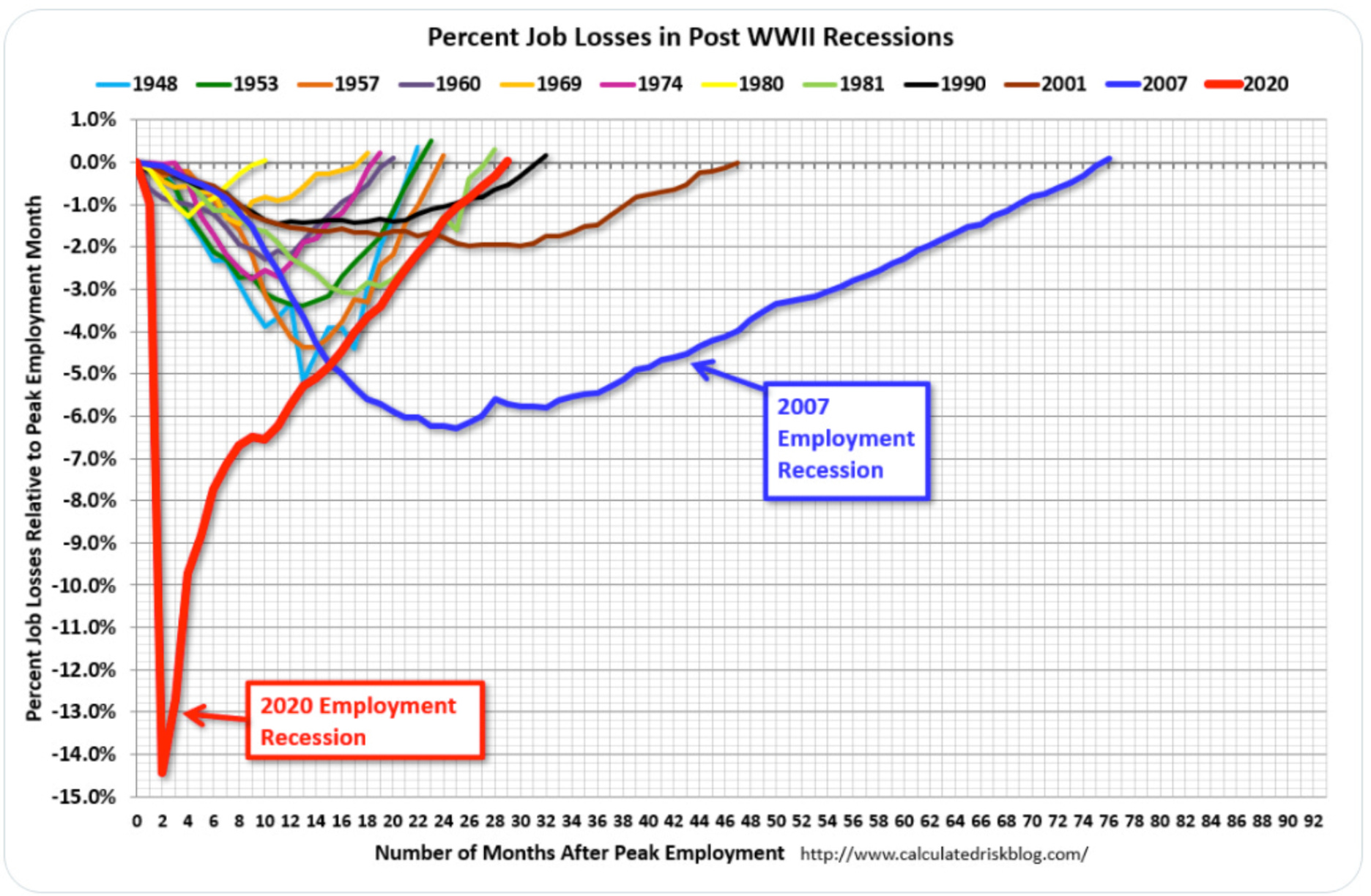

As I showed in this talk, the rebound from the pandemic-induced recession of 2020 has been nothing short of remarkable. Fiscal policy erased the calamitous loss of 22 million jobs at breakneck speed. All of that stuff you’re hearing about Bidenomics— the resilient consumer, reinvigorated business investment, the strength of the labor market—that’s the result of Big Fiscal, my friend.

In case you need a reminder, the bulk of the fiscal response happened in 2020/21:

When the pandemic hit in early 2020, Congress quickly delivered a robust $2.2 trillion fiscal package, known as the CARES Act. That bill was signed into law by President Trump on March 27, 2020. Then, in December 2020, lawmakers returned with more fiscal support, passing a $900B consolidated appropriations bill to shore up the economic recovery. A few months later, in March 2021, President Biden signed the $1.9 trillion American Rescue Plan (ARP). What this means is that Congress kicked out ~$5 trillion in roughly one year’s time. And virtually every penny added to the deficit.

But it didn’t stop there.

The bipartisan infrastructure deal (IIJA), the CHIPS and Science Act, and the Inflation Reduction Act (IRA) tripled down on Big Fiscal, adding significant support to the economy. Not only that, the infusion of public money appears to have catalyzed a boom, crowding in a bunch of private sector investment (new factory construction, etc.). With robust demand and inflation continuing to cool, Goldman Sachs (and others) are revising (downward) their assessment of near-term recession risk.

Frying Pans

Another F-word that grabbed headlines this week came to us courtesy of Alex Williams at Employ America. He charted some headline macro data to drive home the point about the benefits of Big Fiscal, dubbing the images Frying Pan charts because of their panhandle shape. You can click through the entire thread here.

And you can read Paul Krugman’s take on the Frying Pan charts here. The striking feature—and the point Alex was trying to drive home—is that we experienced a lost decade following the 2008/09 recession because Congress and the White House failed to meet the moment with sufficient fiscal force. Instead of providing ongoing fiscal support, democrats basically settled for a one-and-done package known as the American Rescue and Recovery Act of 2009. It was nowhere near enough to repair the damage wrought by the collapse of the housing bubble. Why didn’t the Obama administration deploy more fiscal support ? They were afraid of Big Fiscal. As Krugman put it:

Very Serious People of Washington lost interest in job creation in favor of obsessing about the national debt. As a result, we turned to years of fiscal austerity that held the economy back.

And that brings us to our next F-word.

The Fed

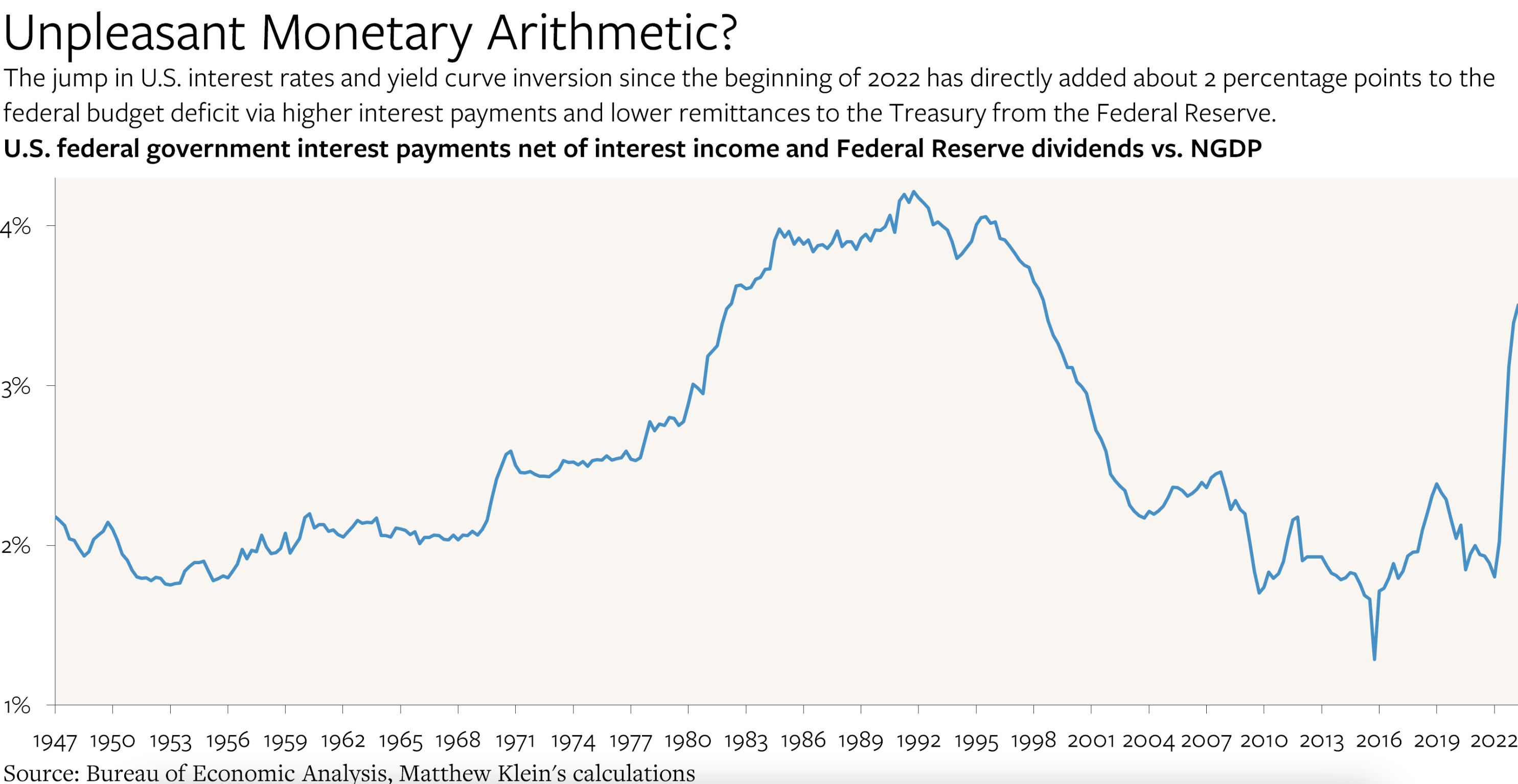

Earlier this week, Matt Klein wrote about the impact of the Fed’s tightening cycle on the federal budget. He recognizes that the Fed’s rate hikes are the main driving force behind the big jump in the government deficit. But Klein doesn’t think it will amount to much (if anything) in the form of added “stimulus” to the economy. It’s a question I grappled with back in February:

At the macro level, the federal government is a net payer of interest, which means that the Fed’s rate hikes work like expansionary fiscal policy in the sense that they translate into hundreds of billions of dollars in additional spending by the federal government.

Within the MMT community, this an argument that is most frequently—and fervently—articulated by Warren Mosler.

Looking at the recent jump in the fiscal deficit (as well as projected increases in near-term deficits), Klein shows that the Fed’s rate hikes are the main thing driving the government deficit higher.

{kind=link}

Mosler argues that this is helping to support the recovery by funneling hundreds of billions of dollars—above and beyond what the government would have paid out in the absence of the rate hikes—to banks (in the form of interest on reserves) and holders of US government bonds each year. In this respect, Mosler insists that the rate hikes, which are supposed to reduce inflationary pressures by serving as a drag on economic activity, are providing an additional source of fiscal stimulus. At least for now. As I wrote back in February:

Mosler acknowledges that rate hikes create both winners (who have more to spend) and losers (who curtail spending). What matters is the balance of these opposing forces. And right now, he thinks the rate hikes are doing more to support aggregate demand than most people—especially central banks—realize.

Klein highlights the substantial boost to private sector income, but he dismisses the possibility that the widening fiscal deficit will induce meaningful increases in consumption spending. He writes:

The downturn in revenues is mostly attributable to the plunge in capital gains tax receipts after the windfall of 2021/2022, as well as the collapse in dividends paid by the Federal Reserve to the Treasury. Meanwhile, the increase in outlays is almost entirely attributable to the surge in interest payments on Treasury debt. Lower taxes and higher spending are boosting private sector disposable income, but this attribution suggests that the beneficiaries will not use much if any of the extra cash to pay for goods, services, or real assets. The “stimulative” impact is therefore likely to be much smaller than what might be expected based on the headline numbers.

As a result, Klein concludes that “There is no ‘stealth fiscal stimulus’” coming from the (mostly) rate-hike-induced spike in the federal budget deficit. Because he doesn’t think the 2 percentage point jump in the deficit will spawn much additional spending, he writes that “none of this is likely to boost PCE.” If that’s all correct, then it’s reassuring to those of us who worry not about projections of widening fiscal deficits per se but about any heightened inflation risk they might pose.

Yet Klein joins a growing chorus of deficit alarmists, writing:

But other perspectives appear more alarming. Comparing January-June 2022 with January-June 2023 shows outlays up by 15% while receipts are down by 14%. Compared to January-June 2019, outlays are up by 48% (10% a year, on average) while receipts are up by only 30% (7% a year, on average).¹ The result is that the January-June deficit has gone from $428 billion in 2019 to $137 billion in 2022 to $971 billion by 2023. Put another way, the year-to-date budget deficit is about 2.3x what it was in 2019, while nominal GDP in 2023H1 was only 26% higher than in 2019H1.

To get me exorcised about the path of projected fiscal deficits, I would need to see credible evidence of a longer run inflation problem. It’s not impossible, but I don’t see it. What I see right now is a fiscal stance that is allowing the economy to sustain low levels of unemployment alongside a continuous deceleration in inflation. To me, that is neither alarming nor evidence of a fiscally unsustainable path.

But the rate hikes, especially if they were to continue, could throw a wrench into what at present remains a pretty happy macro story.1 As MMT economist Bill Mitchell recently wrote:

Trying to work out what the impacts of rising interest rates will be involves a deeper analysis of the distributional impacts of the hikes.

And central bankers are as unclear of the net effects of their actions as anyone.

Borrowers are hurt, creditors gain.

Those who hold financial assets gain, those with little wealth are hurt.

The net impact depends on a number of factors as outlined above.

It is obvious that the rate hikes have not yet caused recessionary conditions to emerge and that is probably because the winners from the hikes are still spending freely on the basis of their wealth gains, while the lower-income groups are cutting back but not to the same extent.

Eventually, if the rate hikes continue, there will be a rise in unemployment as the spending of the wealthy will reach saturation point.

If and when that happens, the automatic stabilizers will push the fiscal deficit higher. At that point, rising deficits will be ‘alarming’ because they will signal the pain of rising joblessness. If the slowdown is severe enough, and inflation is sufficiently muted, the Fed will respond by cutting rates.

Fitch

And this brings us to our final F-word of the week. As you’re undoubtedly aware, Fitch, one of the three big credit ratings agencies, knocked US Treasuries down a peg, lowering the rating on these default risk-free securities from AAA to AA+. Here’s how Fitch justified the move.

Following the downgrade, I gave a number of interviews, commenting on Fitch’s logic (or lack thereof), including this one with Keren Landman at Vox. MMT economist Bill Mitchell called Fitch’s move “as ridiculous as it is meaningless,” and fixed income analyst Brian Romanchuck wrote this piece, explaining why “credit ratings of floating currency sovereigns are silly.”

To the extent that the downgrade makes any sense at all, it stems from the increasingly erratic posturing around the debt ceiling limit. It is about our willingness—not our ability—to pay our bills. As John T. Harvey of Texas Christian University put it:

Can the US be forced into debt default?

Never. Shame on you, Fitch.

Could the gridlocked, highly-partisan, and dysfunctional US government prevent us from meeting financial obligations we absolutely have the legal and economic ability to meet?

Yes. Shame on us, United States. And for that, the debt is the least of our worries.

Closing Thought

Our closing thought comes from economist Daniela Gabor.

The Fitch downgrade is already emboldening the fiscal scolds, who would have us memory-hole the triumph of Big Fiscal and curtail planet- and life-saving investments in our future. We must not let that happen.

Further reading: https://www.phenomenalworld.org/analysis/global-boiling/

I believe that all the interest rate manipulations by the Fed transfers wealth from labor and small businesses to the class of Oligarchs we've created because of our belief in 'trickle down.' This transfer of wealth has a name, the 'allocative effect.' I really don't understand why the Fed still embraces what was called the 'Treasury View' which was discredited during the Great Depression. But here we are.

"If and when that happens, the automatic stabilizers will push the fiscal deficit higher. "

We need to make more of this simple fact.

The closer the increase in the deficit matches the increase in spending, the more *deflationary* it is.

If a $30bn budget spend increases the deficit by $30bn, then we have a deflation problem.

If a $30bn budget spend causes no change in the deficit, then we're stretching the supply side to the full and need to be careful.

It's the non-'deficit spending' bit of increased spending that is potentially inflationary. Not the 'deficit spending' bit.