How (Not) to Fight Inflation

Straight talk not bravado

Thanks so much for reading The Lens, and welcome to all of my new subscribers. In my last post, I asked, “How Do You Solve a Problem Like Inflation?” For many (probably most) economists, it’s a question with such an obvious answer that it hardly merits inquiry. The central bank will take care of it. It’s their job, and they have the requisite tools to handle any inflation problem.1

Mainstream economists concede that it may take time—monetary policy is thought to operate with long and variable lags—but a credible central bank can always steer inflation back on course if (for any reason) it strays from the desired path.

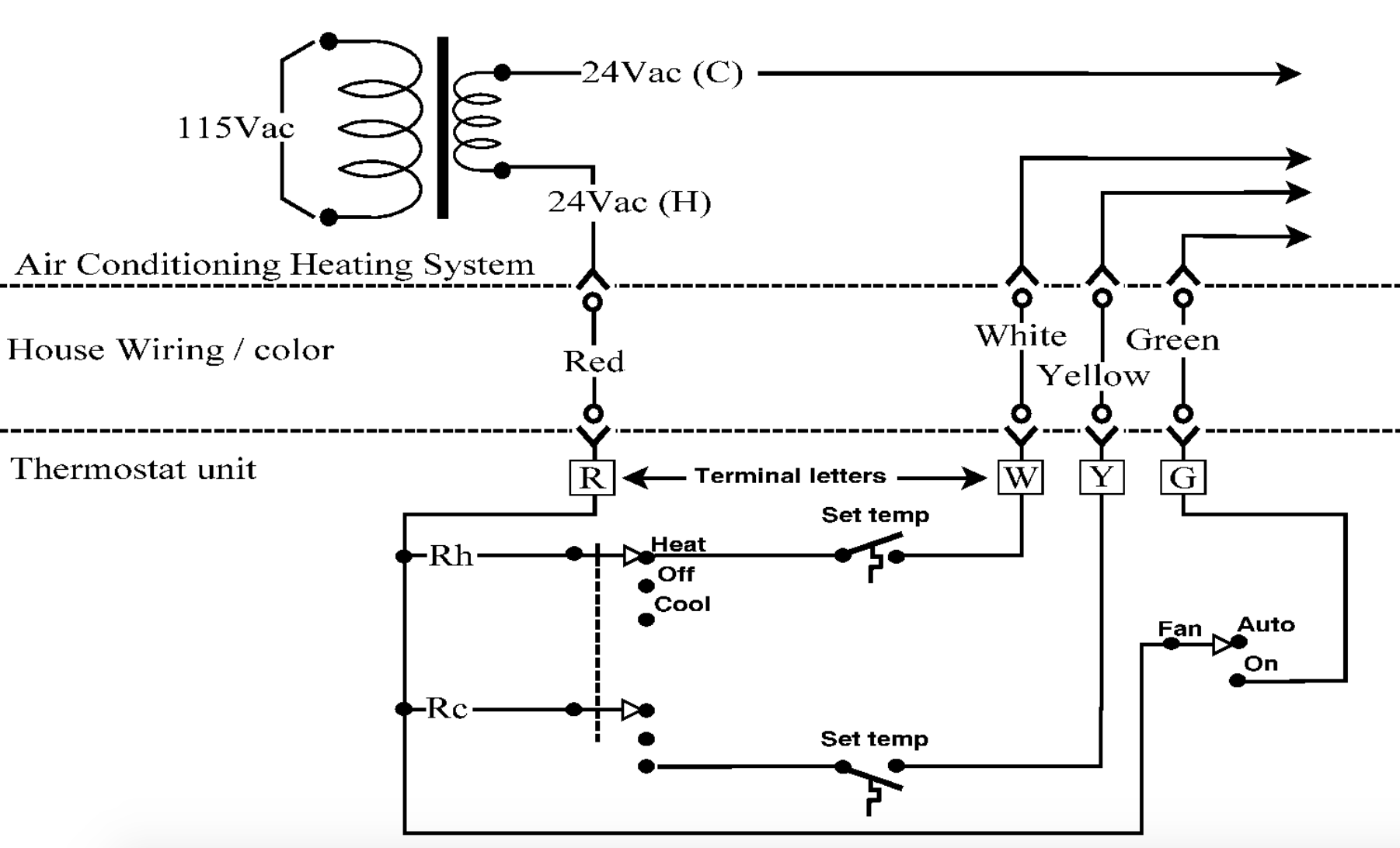

If inflation is considered too low—as it was for so many years following the Global Financial Crisis—the central bank is supposed to dial it up until it reaches 2 percent. And should the reverse challenge arise—like now—the Fed is expected to fix the problem by turning the knobs in the other direction, dialing inflation back down. I talked about all of this with professors James Galbraith and L. Randall Wray in a recent episode of my co-hosted podcast the Best New Ideas in Money. My co-host, Jeremy Olshan, likened the strategy to adjusting the thermostat in your home to achieve the ideal room temperature. That’s a good analogy for how monetary policy is supposed to work. But there’s a reason your thermostat is so dependable. It’s called science.

Your thermostat is wired to your furnace and to the compressor in your air conditioner. The system relies on a thermometer that constantly monitors your room temperature, turning the appropriate unit on/off at just the right moment. It may take a bit longer to cool your space on a really hot day, but with a good system in place, you can always achieve the target temperature simply by adjusting the thermostat.

Unfortunately, our economic system is a lot more complicated. The system isn’t engineered to transmit an impulse—like rising or falling interest rates—through a hard-wired monetary apparatus to a known destination. What actually happens when a central bank dials the interest rate up or down depends on a vast array of unknowables. It’s a point John Maynard Keynes made in one of my favorite passages from The General Theory:

“If, however, we are tempted to assert that money is the drink which stimulates the system to activity, we must remind ourselves that there may be several slips between the cup and the lip.”

At the time, Keynes was making the point that policymakers shouldn’t rely too heavily on central banks to pull the economy out of the doldrums of the Great Depression. He didn’t argue against trying to use monetary policy to help restart the economy, but he understood the inherent uncertainty involved. Increasing the money supply might push interest rates down, and that might induce businesses to borrow and Invest in new plant and equipment, and that might result in higher levels of economic activity.

But there was no guarantee. If liquidity preference2 was running exceptionally high, business sentiment (profit expectations) was rapidly souring, or consumers were scrambling to spend less and save more, then there was no way for the intended monetary stimulus to transmit itself into the form of a hotter economy.

You might be tempted to think that we’ve come a long way since Keynes issued that famous warning. That we’ve engineered a more reliable transmission mechanism so that monetary policy just works better now. That cutting interest rates will always stimulate the economy and raising them will always cool things off. That’s what most economists believe. And it’s what central banks tell us.

Figure 1 comes from the Board of Governors of the Federal Reserve System. The goals are established by Congress in the form of the dual mandate. To deliver on those objectives, the Fed dials interest rates up or down, communicating its intentions—to consumers, the business community, and financial markets—as clearly as possible.3 And then…it waits. And it hopes.

And here’s the European Central Bank’s explanation of how the monetary transmission mechanism is supposed to work.

And for good measure, here’s one from the Reserve Bank of Australia.

Notice how each attempt to explain the monetary transmission mechanism includes the use of directional arrows, just like in the diagram that shows how a thermostat transmits a signal that activates your heating or cooling unit. Except that your electrical system is hard-wired to deliver the same response to any adjustment in the dial, whereas our economic system is enormously complex, subject to any number of breakdowns along the way.

I realize this is tantamount to heresy within the economics profession, where faith in the efficacy of monetary policy runs deep. I simply don’t agree with the sentiment below, and the reasons why have been spelled out by MMT economists like myself in dozens if not hundreds of published papers. L. Randall Wray, alone, has probably published several dozen articles on monetary policy over the last three decades. So the reasons for our skepticism are clear to anyone who cares to do the reading.

And it’s not just MMT economists who are challenging conventional thinking. Here’s Jon Sindreu in The Wall Street Journal, writing Inflation Does’t Have to Mean Higher Interest Rates. And here’s Business Insider’s Alex Yablon explaining why “jacking up interest rates” might not work to fight today’s inflation.

Heck, even the Fed Chairman reminded us in his recent confirmation hearing, that the Federal Reserve’s tools mostly work on the demand side, but the problems we’re facing today are still mainly related to challenges on the supply-side. If that’s correct—and I believe that it is—then it makes it that much harder to see how the impulse of Fed tightening is supposed to transmit itself throughout the system to cool the specific drivers of today’s elevated inflation.

As I keep saying, we need to think harder about inflation. Because in many ways, monetary policy is still flying blind after all these years.

In my last post, I put forward a wide range of policy ideas about how to deal with some of the specific drivers of today’s inflation. There is no silver bullet, but there’s one thing I know for sure: How should we not fight inflation? The answer is cavalierly.

This is what Paul Krugman argued yesterday. His assessment is that labor markets are looking increasingly tight and so with headline inflation running at 7 percent, “it’s time for policymakers to pivot away from stimulus — in particular, that the Federal Reserve is right to be planning to raise interest rates in the months ahead.”

To fight against today’s elevated inflation, the Fed is expected to pair a series of interest rate hikes with an accelerated tapering of its bond-buying program (already underway) followed by some unwinding (or runoff) on its balance sheet.

Matt Stoller wrote a piece on December 29, 2021 in which he estimates that up to 60% of the current inflation (6.8% for 2021) is caused by monopolies/oligopolies raising prices far beyond their increased costs. They have pricing power and they are using it to massively increase their margins. He uses an interesting methodology that makes sense to me, but I would have difficulty describing it as well as he does. For those interested you can find it here:

https://mattstoller.substack.com/p/corporate-profits-drive-60-of-inflation

To the extent that he is correct, neither fiscal nor monetary policy can address this problem. It's going to take re-regulation and a much more robust anti-trust effort by the government. Lina Kahn at the FTC and John(?) Kanter at the DOJ anti-trust division are starting to work on this. Even Congress (amazingly) is getting in on the act by proposing re-regulation of the shipping industry.

I have noted some news items about the impact of climate-induced weather events on the Canadian supply of oil, shipping, trucking, chickens, cattle, vegetables and fruit. I have not followed closely the futures markets for these products but if their availability is being affected negatively, that will cause shortages and likely boost prices without any nominal increase in demand because sellers are able to command higher prices from the more prosperous or middle-class consumers just as the market speculators will bid up their prices.

As you say, inflation is a complex systemic problem with many feedback loops. I also believe that the COVID pandemic has introduced some other costs to retailers for masks, and sanitizing activities that are likely minor factors. In my country, nursing staff are working double shifts meaning overtime rates because of absent colleagues. The price of fossil fuels is affected dramatically by several factors and whereas last summer I was paying less than $1.15 per litre, now I am paying $1.34-6 per litre and as high as $1.46 per litre in Toronto last week.

The notion mentioned in the post by Wally Grigo about too much money chasing too few goods holds water ONLY if the savings rate is starting to decline. Do we have such data? The data that I have seen is that in my country the savings rate has soared to over 30% from around 3%. His idea to have prices take it away would be revealed if savings rates decline. Well-to-do folks complain about inflation NOT because of prices of goods but because of lower returns on investments such as loans and mortgages. As one of those, I notice it at the gas pump but take little notice in the grocery store.

My memory may not be allowing for accurate numbers but the concepts remain valid.