Don't Call it a Q-Turn

And don't call it a "fiscal rescue" either. The BOE's latest move was about rescuing pension funds, not fiscal policymakers.

Early this morning, the Bank of England (BOE) released the following statement. Before we talk about the reason(s) for the intervention, let’s summarize the announcement.

Beginning today and continuing through October 14, the BOE will “make temporary and targeted purchases in the gilt market…at an urgent pace.” So the central bank is once again buying government bonds. This has some people postulating the return of Quantitative Easing (QE). But, wait, there’s more!

The BOE was supposed to be unwinding its balance sheet, via Quantitative Tightening (QT). The BOE says that will still happen, but the sales that were “due to commence next week” will be postponed until Halloween.

Boo!

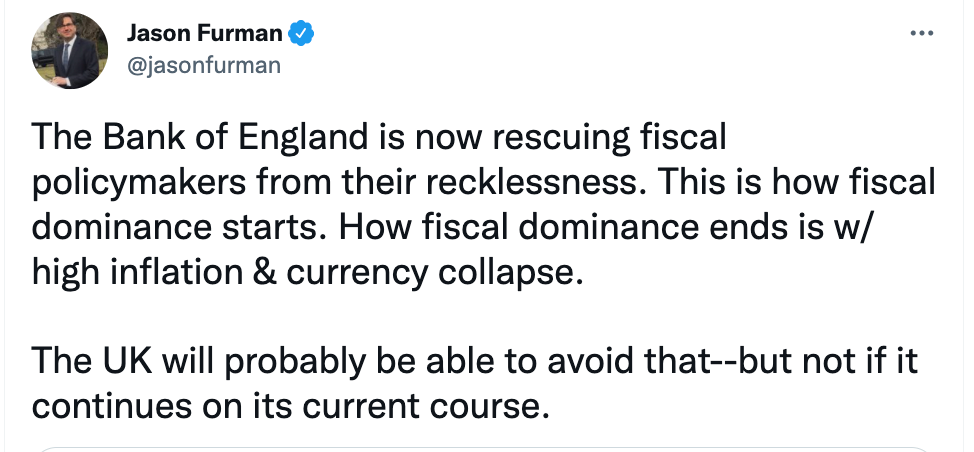

This is apparently a very big and scary move. The BOE is being submissive! Earlier this morning, CNBC’s Becky Quick was quick to read aloud this tweet from economist Jason Furman. Meanwhile, her co-host, Joe Kernan, accused the central bank of demonstrating a lack of resolve on the inflation front, calling the decision to intervene in bond markets “a bonafide blink”. This is called “losing the plot.”

What would a more sober-minded take on the BOE’s statement look like? Here’s how MMT scholar, Nathan Tankus, reacted to the announcement:

Nathan’s point is that the central bank isn’t stepping up to “rescue fiscal policymakers.” It is stepping in to maintain order in the gilt market. (You can argue that the intervention wouldn’t have been necessary but for the “reckless” Truss/Kwarteng mini-budget. And I’ll come to that.) But let’s recognize that the BOE acted in order to resolve dysfunction in the bond market, and that these kinds of interventions are quite normal and routine, not a prelude to so-called “fiscal dominance.” As the BOE explained:

These purchases…are intended to tackle a specific problem in the long-dated government bond market…

The purpose of these purchases will be to restore orderly market conditions. The purchases will be carried out on whatever scale is necessary to effect this outcome.

By now, it seems clear that the real impetus for the intervention was the fact that the surge in interest rates on gilt-edged bonds was about to wreak havoc on UK pensions, which were getting hit with huge margin calls. So it was a a technical move to head off a pension fund calamity. I was talking about all of this with MMT scholar and bond market expert Brian Romanchuk early this morning. Commenting on Furman’s tweet, Brian told me:

Today’s action is an intervention to restore orderly markets. They are ‘bailing out’ anyone hit by margin calls.

There’s a lot of confusion and consternation out there. To the extent possible, I recommend tuning out the hyperbolic pronouncements about “fiscal dominance” and the “doom loop” prognostications about the inevitable collapse of the British pound. Jon Sindrew of The Wall Street Journal has written a very good piece.

Notice that is last point is precisely what I argued in this Lens column just the other day:

[The UK is] the issuer of the that sovereign currency. So it really comes down to the exchange rate—not “funding” per se.

To learn more about the bond market reaction to the Truss/Kwarteng mini-budget and so-called “fiscal dominance,” check out Brian Romanchuck’s latest blog post. And whatever you do, don’t call the latest bond market intervention QE. It will rile up the good folks on #FinanceTwitter.

Posted the below on my Facebook page today. I would add that for most of us lay people, the differentiation between QE or 'bond buying to correct market turbulence', is semantics when the main issue is that, at full employment, the markets - and journalists - now need Ministries of Productivity to publish their strategies BEFORE programmes to spend money into existance are announced.

"As the Thatcher Monetary Orthodoxy disintegrates, why instead do we now need a Ministry for Productivity? Because if you treat people with respect and assume that they are working as hard as they can, in both the private and public sectors; if you agree that the labour market is tight, with unemployment at a near record low; then you also know that no government can spend new money, in these circumstances, without causing inflation; all new spending must be directed to the measures, machines, software, infrastructure and deregulation to unleash sufficient productivity growth to offset the new spending. That is the principal lesson of MMT, Modern Monetary Theory. Stephanie Kelton is brilliant. She changed my mind. Will she change yours?"

Interesting to see that Bond Vigilantes have resumed publication.....and are calling out the threat of long term bond yields on the pension industry in the UK as the basis for the Bank of England intervention.