Reactions to Fed Chair Powell's Speech

Like many of you, I watched Fed Chair Jerome Powell deliver his Jackson Hole speech this morning. It was short (though longer than last year’s) and mostly predictable. I wrote this post last week, noting:

I think it’s pretty easy to anticipate what Powell will say at this year’s gathering. We’ve made substantial progress. But there is more work to do. We are firmly committed to brining inflation all the way back down to 2 percent. We’re not going to declare victory and go fishing.

And that’s pretty much what we got. My own read is that Powell’s remarks leaned hawkish overall. So far, the market response is relatively muted. Nothing like the meltdown that followed last year’s uber-hawkish Pain Speech.

So What Did We Hear?

The Fed Chair repeated that it is the job of the Federal Reserve “to bring inflation down to 2 percent, and we will do so.” He noted that “inflation has come down roughly in line with global trends.” He made it clear that the Fed isn’t satisfied with where we are, and he said that “the process [of bringing down inflation] still has a long way to go.”

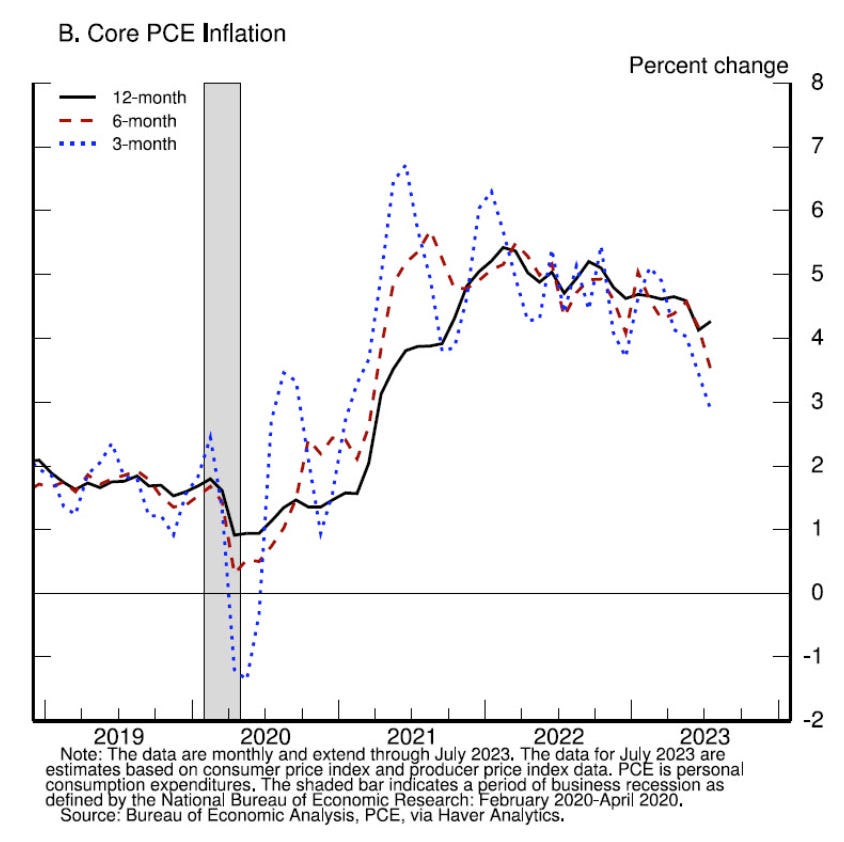

He noted the substantial progress in headline inflation (which has come down from its peak of 9.1 percent in June 2022 to 3.2 percent in the latest reading), but he added that “food and energy prices are influenced by global factors that remain volatile, and can provide a misleading signal of where inflation is headed.” So he mostly focused on core PCE, which is the Fed’s primary inflation target.

The text of the speech wasn’t made public until after his live remarks, so he raised some eyebrows when he said, “Core PCE inflation peaked at 5.4 in February 22 and declined gradually to 4.3 in July.” As JPMorgan’s David Kelly noted immediately following the speech, we won’t have July core PCE data from the BEA until 8:30 a.m. EDT on August 31. The last official read (June) came in at 4.1 percent.

But the text of the speech makes clear that 4.3 percent is the Fed’s estimate for July core PCE.

Looking at monthly data on core PCE, Powell said that “the lower monthly readings for core inflation in June [actual] and July [forecast] were welcome” but “only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal.” He described the outlook as “unclear” with respect to where underlying inflation will settle and that there is “substantial further ground” to get back to price stability.

And then he walked us through what’s been happening with the three broad components of core PCE inflation—inflation for goods, for housing services, and for all other services, sometimes referred to core services ex-housing. I won’t repeat it all here, you can read those passages of the speech or listen for yourself.

The hawkish tenor basically emanates from Powell’s observation that “the economy may not be cooling as expected.” He emphasized that GDP growth is running above trend and consumer spending has been “especially robust.” And even with the backup in long-term yields and the spike in mortgage rates, Powell recognized that the “housing sector is showing signs of picking back up.” He’s worried that all of this “could put further progress on inflation at risk and could warrant further tightening of monetary policy.”

Bottom line? Calls for a higher inflation target have fallen on deaf ears. Powell insists that the Fed can’t stop/won’t stop until inflation is all the way back down to 2 percent. It is an extremist policy commitment.

Getting inflation sustainably back down to 2 percent is expected to require a period of below-trend economic growth as well as some softening in labor market conditions.

Two percent is and will remain our inflation target.

The discussion then turned to real rates, which Powell notes “are positive and well above estimates of neutral.” This tells Powell that monetary policy is currently “restrictive” and it will need to stay restrictive until the Fed is convinced that inflation is on a durable path back down to 2 percent. The problem, Powell admits, is that “we cannot identify with certainty the neutral rate of interest,” nor does the Fed know how much “drag [is] in the pipeline” yet to be felt due to the variability of lags.

He closed with another nod to uncertainty and a commitment to “keep at it until the job is done.”

Conclusion

My read on Powell’s read of the inflation outlook is that the Fed continues to believe—despite any evidence—that core services ex-housing (and in particular wage growth) could cause inflation to become persistent. The reality is that there aren’t that many parts of the economy that are very sensitive to interest rates, and inflation has mostly come down for reasons unrelated to tightening monetary policy.

It takes time for all of the elevated drivers of inflationary pressure to pass through and show up in the data. But it is happening. Patience is what we need, but the Fed appears committed to an extremist strategy in order to get all the way back to 2 percent inflation. As David Kelly noted this morning, that is an extremist commitment that risks sacrificing 1.6 million people at the alter of getting to 2 percent. “This is not,” as Kelley put it, “an inflation prone economy.”

Who in their right mind wouldn’t prefer an economy with 3.5 percent unemployment and 3 percent inflation to a collapse in the housing market and a full-blown recession?

Further to Stephanie's diplomatic and deliberately restrained comments on Chairman Powell's recent speech I would like to add a few more relevant comments.

It should be clear to all of us by now that the objective of the deficit hawks in the Fed ACTUALLY IS to raise unemployment, increase personal and business bankruptcies and to weaken those parts of the economy where the general public and main street live and transact. The deficit hawks are partially attaining that objective.

It looks obvious to me that fighting inflation is just a convenient pretext for the Fed and it's Chairman, although they like most people would no doubt prefer low inflation to high inflation over the long term.

Inflation is however being successfully fought by the Biden administration and by the EU through direct action for example by increasing supply from alternative oil and gas sources (US strategic petroleum reserve releases and increased US and global fracked (mostly) gas and LNG supplies) and by reducing oil and gas demand (energy conservation and more renewable power plus more coal fired power especially in Europe as Russian oil and gas supplies to Europe wind down). China's manufacturing powerhouse has also come back online thus relieving many shortages that arose from the recent pandemic.

Similarly Ukraine via the mechanism of the Grain Deal with Russia was recently able for many months to export their agricultural commodities in large quantities following Putin's messianic invasion, thus relieving some of those associated global commodity shortages. Russia has been a big exporter of those same commodities thus helping to unwind some of their own (Putin's) damage.

Spain even successfully managed to impose price controls on profit gouging corporations thus reducing that major source of inflation at least in that country. In most countries wage increases have not kept pace with inflation so this has had a major deflationary effect.

A truly major oil and gas supply shock potentially worse than the two Middle East oil supply shocks of the 1970's (firstly OPEC's huge oil price increases in 1973 following the Yom Kippur War and later the Iranian Revolution in 1979) appears to have been successfully averted primarily by the US, the EU and by many other global energy exporters. All of this came so soon after that other huge economic shock – the global Covid-19 pandemic that was defeated mainly through national central bank currency issuance on a unprecedented scale.

Stephanie and the MMT fraternity through their educational and publicity efforts and through the soundness of the economic theories themselves have no doubt been at the heart of these major successes, even if they have often felt like tiny voices in a storm of misinformation and lies.

Bill Mitchell's blog posts on Japan show how inflation can be restrained very successfully with minimal pain for the general public and for the productive business sector over this challenging period. The rest of the world could and should have done much the same wherever appropriate.

Japan’s monetary policy experiment is working – Bill Mitchell – 26 June 2023

https://billmitchell.org/blog/?p=60938

Monetary policy in the hands of the central banker sociopaths is advancing the class interests of the elites – Bill Mitchell – 5 July 2023

https://billmitchell.org/blog/?p=60960

Logic and the legitimate objectives of social justice, serving the public interest and good public administration should dictate that deficit hawks, neoclassical (and related) economists and 'free market/small or zero government' zealots should be dismissed from their positions in government and from any important governmental agencies such as the Fed.

It is now clear as day to me that Powell is not acting on behalf of the general public or of the productive portion of the business sector but presumably for the banking and finance elites from which he and his associates were spawned - Wall Street's vulture bankers that no doubt crave another opportunity to feed on some bargains in the event of a successfully engineered economic downturn.

This all sounds like a re-run of the 2008 -2009 GFC or Great Recession to me which was in many key ways a rerun of Paul Volcker's shock therapy and the associated evisceration of the US and global economies starting in 1981 and 1982 and the ten lost 'Volcker years' period that must NEVER BE REPEATED.

Matt Taibbi's famous article appears to be very apt again.

The Great American Bubble Machine – Matt Taibbi – Rolling Stone – 5 April 2010

https://www.rollingstone.com/politics/politics-news/the-great-american-bubble-machine-195229/

Biden and much of Congress appear to be learning to be deficit doves or maybe even to be deficit owls and appear to be winning their joust with Powell and some other allied dangerous 'experts' like Larry Summers but would it not be simpler and be more rational just to remove most of the destructive deficit hawks and similar neoliberal free market/small government fundamentalists and scammers from public office as after all they have been working for the partisan interests of someone else all along?

Why doesn’t President Biden fire Powell and replace him with someone who has the entire country’s best interest in mind and not just the wealthy ?